Healthcare

Capital Markets

|

|

|

|

|

|

|

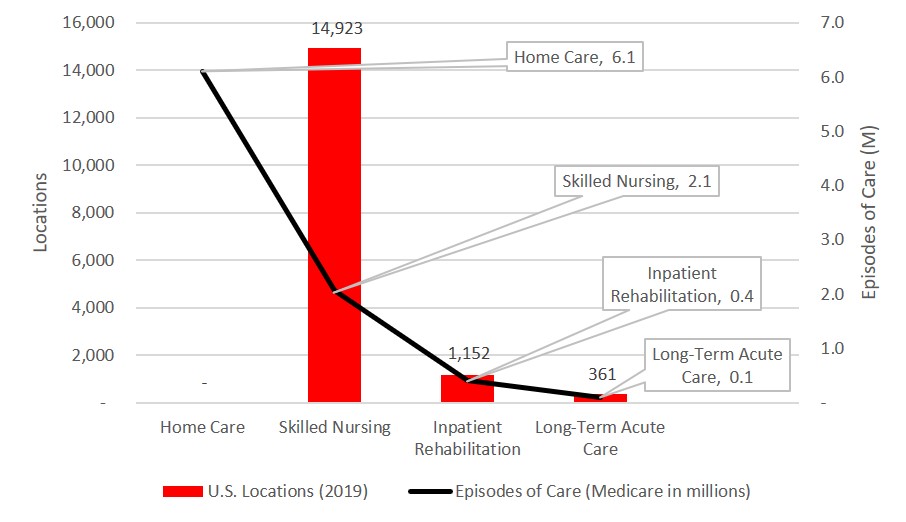

Post-acute care trends drive lower cost and convenient settings

Post-acute settings and episodes of care, 2019

|

|

|

|

Source: MedPAC Report to the Congress, March 2021

|

|

|

|

Key points:

- Post-acute care plays a vital role in patient recovery following release from a short-stay hospital. Rehabilitation treatment, designed to each patient’s unique care plan, is intended to avoid further health complications and possible hospital re-admission. Given that 44% of hospital patients are discharged with a post-acute care requirement, the need for rehabilitation and/or admission to a post-acute inpatient hospital facility is significant. The modalities of care span a broad range, with in-home post-discharge care on one end and long-term acute care facility admission on the other.

- Variation within this spectrum of care includes outpatient rehabilitation as a complement to home care; skilled nursing facility residential care; and admission to an inpatient rehabilitation hospital (IRF) or long-term acute care hospital (LTACH). Reimbursement and eligibility requirements, which are driven by Medicare regulations, are the primary determinant of the destination of care, with costs rising alongside the spectrum of acuity. For example, skilled nursing rehabilitation is the lowest level of acute residential care and provides 1-hour of therapy a day, while IRF admission requires patients to sustain 3 hours of active therapy a day. Finally, admission to LTACHs typically involves patients requiring medical intervention such as respirators, dialysis, transfusions, and advanced wound care.

- Current healthcare trends have influenced a migration of care toward lower cost settings, led by the gradual Medicare reimbursement shift away from facility type and toward diagnosis and rehabilitation requirement independent of site of care. Further, the Centers for Medicaid and Medicare Services (CMS) has identified post-acute inpatient care as an area for rationalization of services. Post-acute care reimbursed by Medicare was $58.5 billion in 2018, the most recent year for which data is provided, representing 10% of the 2018 Medicare budget.

- Post-acute care is growing at a rapid rate, fueled by the robust increase in the over-65 population, which represents 70% of reimbursements associated with these facilities. Advances in technology and home monitoring, along with Medicare reimbursement changes, have increasingly guided discharges toward lower acuity settings, particularly to home health care with follow-on outpatient therapy.

- Illustrating this point, home health care for Medicare beneficiaries rose by a remarkable 50% between 2002 to 2019, from 4.1 million episodes of care to 6.1 million; this outsized growth caused home and outpatient rehabilitation therapy to dominate the post-acute treatment category, at 47% of all post-acute care. Rehabilitation in skilled nursing facilities is the second most frequent setting of care, with nearly 2.1 million episodes amongst Medicare beneficiaries in 2019 provided at approximately 15,000 locations around the country. Inpatient rehabilitation at IRFs is limited to 1,152 hospitals in 2019, approximately the same number of facilities in the past decade; however, caseload increased by 12% during this time, rising from 365,100 cases in 2010 to 409,000 cases in 2019. Because of the CMS policy change towards site neutrality, LTACHs are least in favor, with a declining number of facilities – 361 in 2019 vs. 421 in 2012 – and an annual compounded case loss of 10.1% from 2016 to 2019.

- The recent changes in regulatory and reimbursement policy reflect advances in technology as well as the delivery of post-acute care. While the delivery of care remains focused on the promotion of functional ability following discharge from the hospital and the avoidance of re-admission, new strides in technology can achieve care delivery in a more cost-efficient manner.

|

|

|

|

New Listing - Investment Sale

|

|

Legacy Oaks

227,657 s.f.

San Antonio, TX

|

New Listing - Investment Sale

|

|

The Keith Corp MOB Portfolio

72,499 s.f.

Charlotte, NC

|

New Listing - Investment Sale

|

|

Kansas City Net Lease Medical Office Portfolio

50,469 s.f.

Kansas City, KS-MO

|

|

|

|

Closed - Investment Sale

.

|

|

Palomar Health Outpatient Centers – Phase II

75,000 s.f.

San Diego MSA

|

|

|

Closed - Investment Sale & Debt Placement

|

|

Bellaire Medical Plaza

58,517 s.f.

Houston, TX

|

Closed - Investment Sale

.

|

|

The Laguna

57,573 s.f.

Laguna Hills, CA

|

|

|

|

Closed - Investment Sale

.

|

|

Georgia Bone & Joint

59,550 s.f.

Cartersville, GA

|

|

|

Closed - Investment Sale

.

|

|

Westover Hills

29,375 s.f.

San Antonio, TX

|

Closed - Investment Sale & Debt Placement

|

|

101 Laguna

21,554 s.f.

Fullerton, CA

|

|

|

|

|

|

|

55-01 Myrtle Avenue

21,154 s.f.

Ridgewood, NY

|

|

|

|

|

|

9500 North Central Expressway

20,296 s.f.

Dallas, TX

|

|

|

|

Serenity at Summit – South Building

18,954 s.f.

Haverhill, MA

|

|

|

|

|

|

|

PM Pediatrics

5,051 s.f.

Mount Prospect, IL

|

|

|

|

|

|

|

|

Want to receive more deal opportunities? Register for the JLL Investor Center, our new portal offering secure and easy access to our global inventory of investment opportunities.

From any device, anywhere in the world, you can search and view listings, receive invitations to private listings, and edit your preferences so you only receive opportunities that meet your specific criteria. Register for the Investor Center here>

|

|

|

|

|